A lack of access to finance holds back economic growth, because firms are unable to seize profitable investment opportunities. A well-functioning market for corporate financing is a key component of the monetary transmission mechanism.

By Peter Praet

On 28 and 29 November, the European Investment Bank and the European Central Bank, in cooperation with the Massachusetts Institute of Technology, Columbia University and SUERF (the European Monetary and Finance Forum) will co-organise a high-level conference on ‘Investment, Technological Transformation and Skills’.

When the sovereign debt crisis unfolded in 2011 and 2012, firms encountered substantial difficulties in obtaining funds from external sources. The conditions for both market-based and bank-based financing deteriorated, particularly in the countries that were most affected by the crisis. Corporate bond spreads widened and the interest rates on corporate loans increased. Credit applications were more likely to be rejected or were discouraged in the first place. The impaired access to finance caused a slowdown in business investment and was a factor in unleashing recessionary and disinflationary forces in the euro area.

The broad range of unconventional monetary policy measures adopted by the European Central Bank helped to restore and strengthen firms’ access to finance. For example, the conditions attached to the targeted longer-term refinancing operations incentivised banks to lend to non-financial corporations. Other ECB measures, such as the negative deposit facility rate or the asset purchase programme, also had a positive impact on firms’ funding conditions: they induced banks to rebalance their portfolios and expand their lending activities.

The corporate sector purchase programme (CSPP) improved the market-based financing conditions of all corporations irrespective of whether their bonds were eligible for the programme. Announced in March 2016, it comprises purchases of investment-grade euro-denominated bonds issued by non-bank corporations. ECB research 1 shows that the CSPP improved the conditions for market-based financing for firms in the euro area: in the year following the CSPP announcement, the spread between corporate bond rates and risk-free rates narrowed by 25 basis points for CSPP-eligible bonds. As investors rebalanced their portfolios and demand for other corporate bonds increased, spreads on ineligible corporate bonds also declined by 20 basis points. The CSPP alleviated market-based financing conditions beyond the scope of targeted corporate securities.

The easing of conditions for market-based financing spilled over to the corporate loan market, improving access to bank funding for small and medium-sized enterprises (SMEs). The CSPP induced firms with access to bond markets to replace bank loans with newly-issued bonds. This shift from bank-based to market-based financing freed banks’ balance sheet capacity, allowing them to expand their lending activity. The increase in loan supply particularly benefited SMEs as they predominantly finance themselves through bank loans.

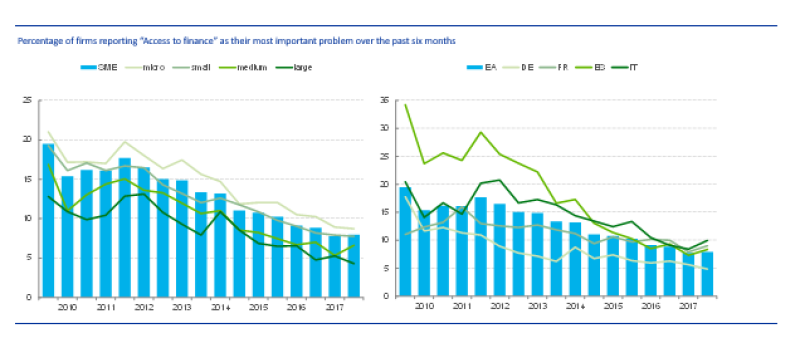

The ECB’s unconventional monetary policy measures helped to continuously improve access to finance for SMEs. In 2009 almost 20% of SMEs in the euro area viewed access to finance as their most important problem, but that share had steadily declined to 8% by 2017. 2 Chart 1 shows that corporate financing conditions improved for firms of all sizes across the euro area.

Chart 1: Access to finance as the most important problem

Base: All enterprises. Figures refer to rounds three (March-September 2010) to eighteen (October 2017-March 2018) of the survey.

Left panel shows results for different firm sizes. Right panel shows results for different countries.

Source: SAFE survey, March 2018.

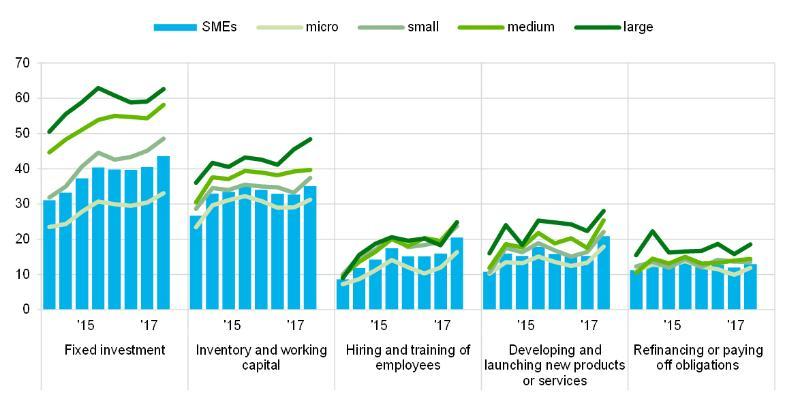

As financing conditions improved, firms invested more in fixed capital and in hiring and training employees. Improved financing conditions had real effects on firms’ investment decisions. SMEs used the easier access to funds to invest more in new property, plant and equipment (see Chart 2). In addition, the share of SMEs investing in the hiring and training of employees increased from 9% in 2009 to 20% in 2017. By contrast, the share of firms that used funds to repay or roll over existing obligations remained stable. The improved access to finance spurred business investment in physical as well as human capital, thereby fostering job creation and supporting growth in the euro area.

Chart 2: Purpose of the financing as reported by euro area enterprises

Base: All enterprises. Figures refer to rounds eleven (April-September 2014) to eighteen (October 2017-March 2018) of the survey.

Note: The figures are based on the new question introduced in round eleven (April-September 2014).

Source: SAFE survey, March 2018

About the author

Peter Praet is a member of the Executive Board of the European Central Bank

Footnotes

- De Santis, Roberto A., Geis, André, Juskaite, Aiste, Cruz, Lia Vaz: “The impact of the corporate sector purchase programme on corporate bond markets and the financing of euro area non-financial corporations”, Economic Bulletin, Issue 3/2018

- The data are based on the Survey on the Access to Finance of Enterprises in the euro area (SAFE). The survey has been conducted biannually by the ECB since 2009 and provides evidence on financing conditions for SMEs as compared with large firms.